- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

Analysis

Market Playbook: Navigating Risks, Nvidia Earnings & FX Trends

Despite the NAS100 and S&P500 still a whisper from ATHs, investment managers spent much of Friday selling winners and profitable long positions – with a clear rotation out of growth and high momentum equity plays, and rolling into the safety of staples, utilities and US Treasuries.

Demand for volatility was also evident from both retail and institutional accounts, and while options expiry (OPEX) and the daily rebalancing of leveraged ETFs played a key role in the moves on the day, there was an obvious demand for ongoing portfolio protection.

The VIX index closed +2.6 vols to 18.21%, with 821k VIX calls trading on the day vs 349k VIX puts. The UVIX ETF (2x long VIX futures ETF) traded a record volume of 17.95m shares. S&P 1-month S&P500 put implied vol (17.37%) pushed to a 5.8 vol premium to call volatility (11.5%).

High short interest names were taken to the woodshed, as were US small caps (the Russell 2k closed -2.94%), while the Mag7 basket closed -2.5%, and were responsible for subtracting the lion's share for the index points. The loss of love for the Mag7 stocks is a big factor and maybe we will see that negative mindset reverse through the week, but it will require Nvidia to hit the sweet spot on Wednesday in its Q425 earnings release. For now, the momentum-based investor flows head to the East to China/HK, as well as into EU defence spend equity beneficiaries.

The Cause of the Selling?

There was no one smoking gun behind the selling on Friday, rather a combination of negative influences, all coming together as one aggregated force - OPEX-based flows, weaker US services PMIs (49.7), Increased University of Michigan 5-10 inflation expectations, reports of a new coronavirus in Chinese media, concerns of a more isolated European defence position and a broad feel that the Mag7 players are lacking a near-term upside catalyst.

The fact the S&P500 and NAS100 closed at session lows also speaks volumes, as Friday’s intraday tape was an out-and-out trend day, with volumes in US equity futures picking up markedly leading into the US cash equity open. It’s clear that buyers simply went missing, with the buy-side funds (hedge funds etc) skewed heavily ‘better to sell’, the high-frequency players sensed the one-sided order book and could execute on shorts with far greater effect.

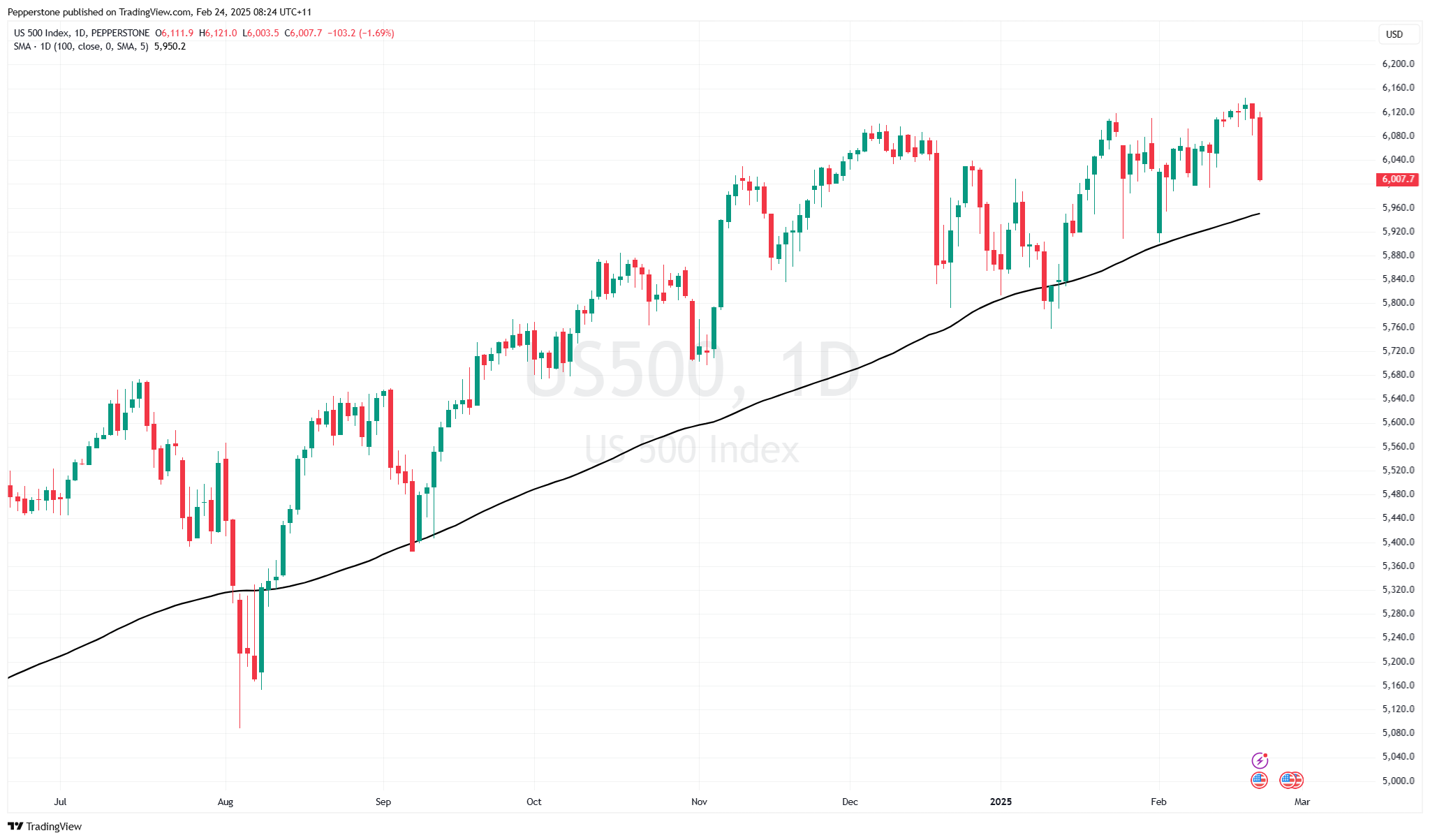

US Equity Indices and Futures Eyeing Big Support Levels

A test and break of the 100-day MA in S&P500 futures (5973), and NAS100 futures (21146) early this week would get markets moving along, and we then start to consider levels where CTAs start to run down longs - weakness breeds weakness. Conversely, we also need to be open-minded to the idea that post-OPEX, the buy-the-dip crew could come back in – Nvidia would likely be at the heart of that reversal, and they will need to hit us with Q425 sales of $38.5b and to guide to $42.5b in sales in Q126, while also offer a strong sense that margins could build in the coming quarters.

Commodities also added to the concerns with WTI crude -3.1% and testing recent lows of $70. 12 – a break here and the recent form in energy equity names will come undone. Copper was also on the radar, closing (on Friday) below recent lows and it's looking like we could see further downside into $4.40.

Navigating the Week Ahead - Event Risk That is Front of Mind

Looking ahead, the bulls will need to monitor for follow-through de-risking in the early throws of the new trading week. Starting the week off and we’ve seen exit polls from the German election offering no real surprises – the CDU/CSU tie-up stops short of the seats needed for a simple majority and will therefore need to reach out to the SPD or the Greens for a coalition partner – the process is glacial, and we may not have a firm answer for 2 months. We’ll see if there is any reaction in the DAX futures (open 11:10 AEDT), but it seems unlikely to overcome the other forces at work in markets.

Asia looks set for a weaker open, with Japan eyed notably weaker, with our JPN225 index closing below the rising trend support it’s held since November - I sense this being a clear target for those wanting to 'sell the weak'. China’s AI/Internet equity plays will continue to be a central focus, but with the technicals now so stretched, these plays are hard to chase at current levels.

By way of event risk – Nvidia’s numbers will be the central focus, as will headlines on Ukraine and how European nations will need to step up to fill the void from reduced future US financial support. China hit us with PMI data, but the data release date falls on Saturday - either way, the PMI data is important as there are increasing signs that momentum in the Chinese economy is building, and this is a key factor offering additional tailwinds to the recent equity outperformance – the sell-off in the Chinese bond market is testament to this view, with the yield on the 5yr govt bond rising from 1.32% to 1.58%.

US core PCE will be the marquee data release on Friday, although the Fed’s preferred inflation gauge is expected to moderate to 2.6% y/y (from 2.8%) and if that eventuates should reinforce the Fed’s skew in policy setting – where an extended pause is the base case, but the next move is still considered to be a cut.

We hear from a raft of Fed speakers, who shouldn't really move the dial too intently on US rates pricing, or the USD. We have seen some worrying readings in the survey-based data (University of Michigan) and short-term breakeven inflation rates have risen strongly, which has pushed US real rates sharply lower (the big kicker behind the USD sell-off), but importantly US longer-term inflation expectations remain well anchored. Dallas Fed President Lorie Logan's speech on Tuesday will perhaps be the most insightful as she touches on the Fed's balance sheet - a factor that gets increased attention in the wake of last week’s FOMC minutes that highlighted that certain members were modelling an earlier end to QT.

The Markets Reaction Function is Sensitive to Negative News

It’s a week where the market could feasibly respond to any economic data point. With US growth concerns building traction, the market’s reaction function is now heavily skewed to any downside in the data outcomes. A downside surprise in the consumer confidence report, or in any of the US regional PMI survey's, durable goods, or possibly even the many housing data releases could trigger a reaction in a market that needs no excuses to de-risk.

For the FX traders, while the sell-off in the USD has been tactically driven by a more benign tariff backdrop and signs that US growth is being called into question, amid an improving economic picture in China, it’s the move lower in US 2-, 5- and 10-real rates that is key behind the USD sell-off. A break this week below 2% in the US 10yr real rate (i.e. 10yr govt bond adjusted for expected inflation) and the USD sell-off will likely continue.

Good luck to all.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.