- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

- Монгол хэл

Inflation Continues To Climb

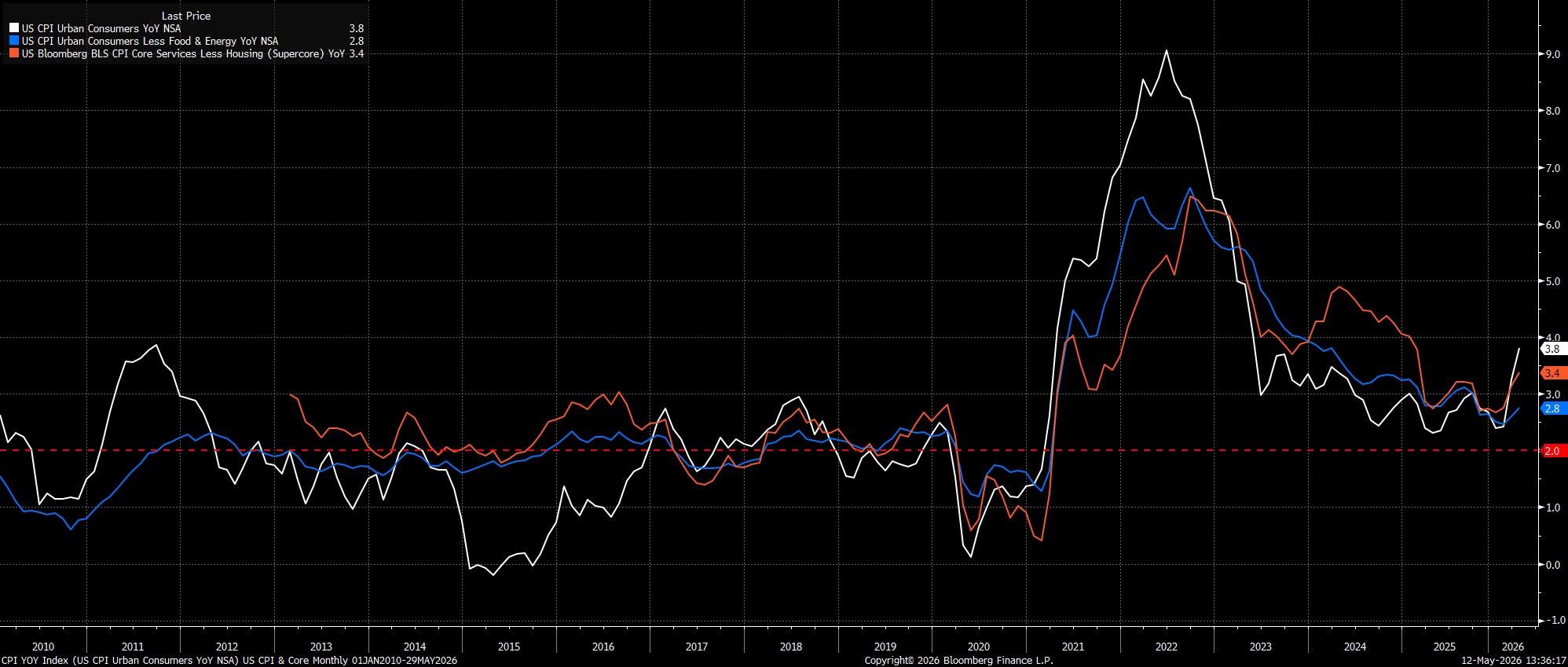

Headline CPI rose 3.8% YoY last month, a touch hotter than consensus expectations for a 3.7% YoY increase, and the fastest annual rate of inflation since May 2023. Once more, as with the March report, the further climb in headline inflation was almost entirely due to energy prices, as normal commodity flows remain hugely disrupted as a result of the effective closure of the Strait of Hormuz.

With the noisy nature of the headline figures in mind, it remains considerably more instructive to examine underlying price metrics. On this note, core CPI (excluding food and energy) rose 2.8% YoY, the fastest pace since last September, while the ‘supercore’ CPI metric (core services ex-housing) rose by 3.4% YoY.

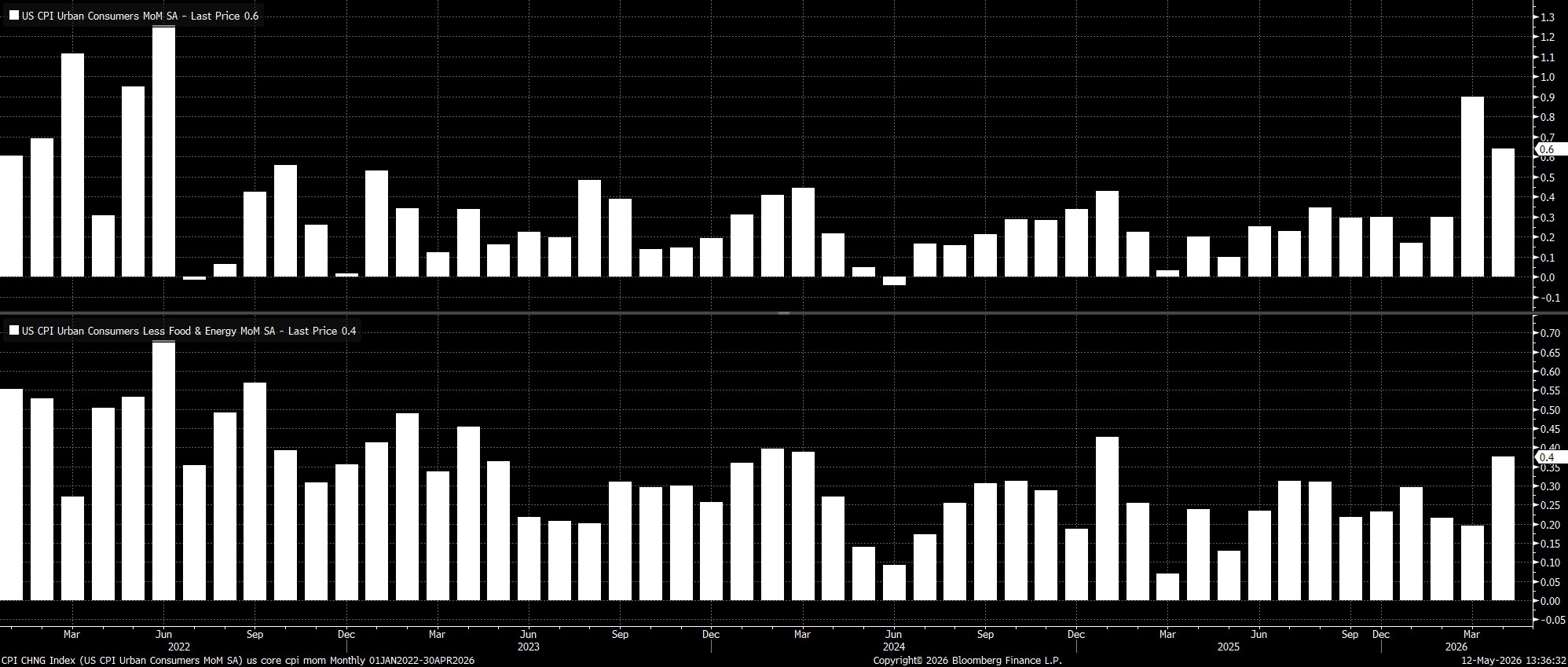

Meanwhile, on a month-on-month basis, the impact of the continued rise in energy prices remains stark. Headline inflation rose 0.6% MoM last month, a touch cooler than the pace seen in March, but still the second fastest annual rate since the middle of 2022. Core CPI, however, predictably remained somewhat more contained, rising 0.4% MoM, roughly in line with the pace seen over much of the last 12 months.

Annualising these MoM figures helps paint a picture of the underlying near-term inflationary trend, even if the headline figures are still skewed higher by the impact of energy:

3-month annualised CPI: 7.3% (prior 5.3%)

3-month annualised core CPI: 3.2% (prior 2.9%)

Devil Remains In The Detail

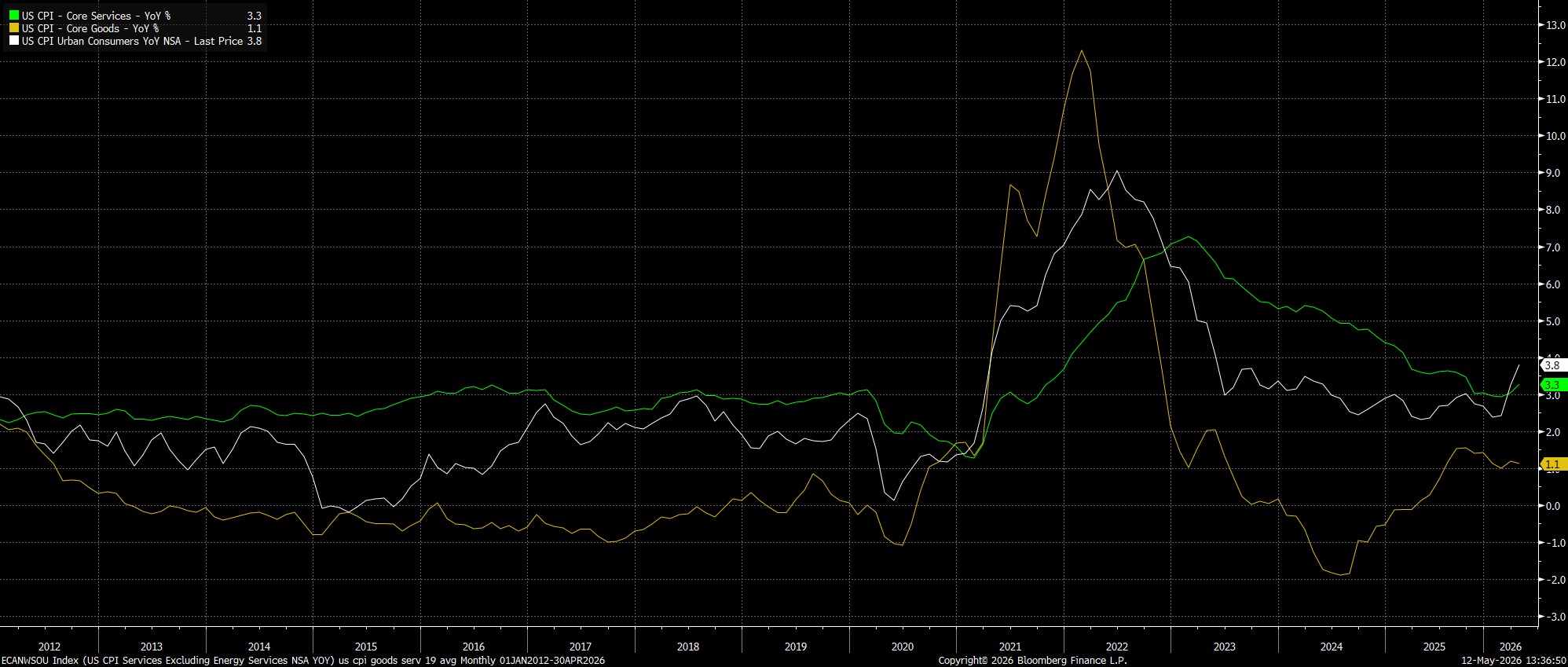

Taking a look under the surface of the report, and as already noted, energy prices were again the main reason for headline inflation having taken another leg higher last month. The sector contributed to around 40% of the MoM increase in headline CPI, with energy prices having risen by 3.8% MoM/17.9% YoY in April.

Setting energy prices to one side, the report also showed core services inflation ticking higher to 3.3% YoY, the fastest pace seen year-to-date, though core goods inflation remained largely unchanged from last time out, at 1.1% YoY.

Money Markets Unchanged

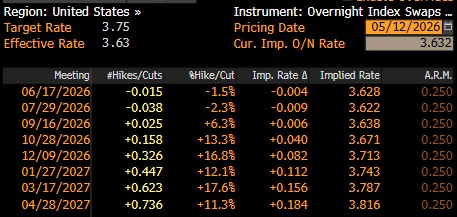

In reaction to the inflation figures, swaps continue to discount around 7bp of tightening from the Fed by year-end, largely unchanged from pre-release levels, though somewhat too hawkish, in my view, as covered below.

Conclusion

For the most part, today’s inflation data tells us relatively little by way of new information. We already knew that energy prices had risen further, and that spot headline inflation would follow suit, which is exactly what has transpired in the April CPI report.

In terms of the FOMC outlook, the rise in headline CPI shan’t move the needle especially much, given policymakers’ continued focus on the both the duration of the energy price shock, as well as the risk of second-round inflation effects emerging. Today’s print provides little clarity on either of those points, though the continued ‘no hire, no fire’ nature of the labour market, as well as the well-anchored nature of long-run inflation expectations, both mean that the risk of second-round effects materialising seems minimal for now.

Looking forwards, the FOMC are likely to retain their ‘wait and see’ approach for the time being, seeking confirmation that the energy-induced rise in inflation will indeed prove to be temporary in nature, before seeking to make any policy adjustments. That said, once such confidence is obtained, there remains a path to the FOMC delivering a cut or two before the end of the year, driven by labour market fragility, with policymakers remaining likely to ‘look through’ any temporary hump in headline inflation for the time being.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.