- English

- 中文版

Analysis

Trading Nvidia - The debate on the future of this momentum juggernaut

In my opinion, AI has only just started to really be incorporated into a wide range of global businesses, where it will deliver significant cost savings and efficiencies. And we only must look at the hundreds of billions of USDs of AI-related CAPEX intension recently announced by Alphabet, Amazon, Meta and Microsoft, to feel confident that this AI has a huge future.

That said, since Nvidia hit an all-time high on 20 June, the share price has been range-bound – with buyers supporting below $100 and selling out of positions above $130.

There is a clear debate in the market on whether valuations have priced in a future that is too optimistic, relative to others who say that further consolidation in the near term is likely before we see another leg higher once the market feels comfortable pricing on the margin story. While the Blackwell GPUs roll out sets a platform for future sales beats.

While this debate rages on, it feels highly probable that the range of $100 to $130 holds in the near term and that could offer a compelling two-way opportunity.

So, we explore the arguments being put forward by both the doubters and the Nvidia bulls.

The Bear Case – What I’m hearing as reasons to be cautious

• After such a strong run, valuations fully discount the consensus 107% of revenue growth in FY2025. While looking ahead, the rate of change in revenue growth is expected to grow at a slower pace, with analysts forecasting revenue growth of 42% in FY2026, 19% in FY 2026 and 12% in FY2028.

• One of the key investment themes has been Nvidia’s incredible gross margins – However, gross margins peaked at 78%, and have started to fall back to 75%. With competition building from AMD, ARM and Intel, Nvidia could be forced to lower prices in the future and margins will be impacted.

• As with any monopoly, there comes government risk, and post the November US election the US administration (whichever party that may be) may limit Nvidia’s pricing power and implement measures to increase competition.

• There has been a growing concern that the hyperscaler businesses (Google, Amazon, Microsoft, Microsoft and Meta), who have invested some 80%-90% of their CAPEX spend into Nvidia’s products, may not get the return on the investment. Nvidia’s next growth phase relies on its key customers seeing clear returns on their CAPEX plans.

• With Nvidia sourcing 90% of its advanced chips from Taiwan Semiconductor (TSMC), there is a tail risk that geopolitical tensions arise between China and Taiwan, which could radically impact Nvidia’s production capacity.

• Nvidia sources 22% of its revenue from China, so should Trump become President in November we could see Nvidia’s revenue impacted by deteriorating US-China trade relations.

The bull case – The argument I’m hearing for renewed upside in the share price

• Having fallen 25% from the June highs, the drawdown into $100 offered a compelling entry point and we’re already seeing signs of funds chasing the rebound into $119.

• Blackwell GPUs will be supplied in 2025, and the market will likely “buy the fact” when the first deliveries are made.

• Granted, margins have peaked and will fall further, but the bears are too pessimistic and when the market feels comfortable that gross margins should trough around 73%, then the share price should break to new highs.

• CEO Jensen Huang spoke at the Goldman Sachs tech conference (on 12 Sept) and detailed that the demand for its products is so great that customers are becoming “emotional”.

• Huang also laid out the idea that any supply issues relating to TSMC could be solved by moving to other suppliers. Huang also addressed the issue of the hyperscalers getting a return on their capex plans and laid out that there will be a huge replacement exercise in the years ahead to replace the CPU-driven data centres.

• While competition will increase in the GPU space, Nvidia has the talent and balance sheet to evolve and stay ahead of the pack, creating faster and more innovative products.

• If we do see a recession in the US, Nvidia will likely be impacted by the broad negative sentiment, but earnings should be far less impacted than many economic-sensitive stocks.

• News that OpenAI is raising $6.5b on a $150 billion valuation supports Nvidia – where we consider that OpenAI allowed employees to sell down their equity in February at a valuation of $86b. That’s an impressive increase and suggests the AI space is still hot.

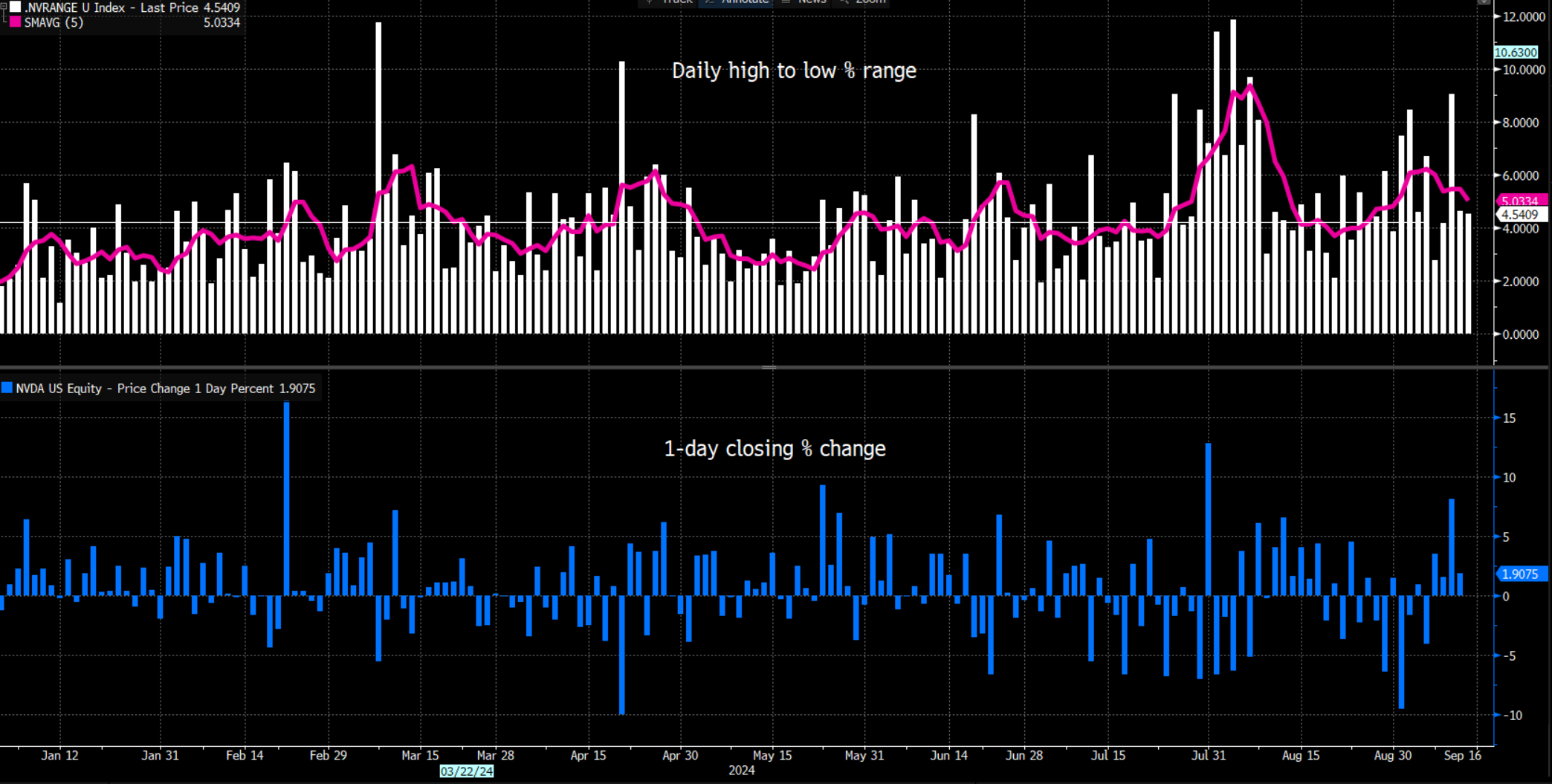

Nvidia: An exceptional trading vehicle

In the past 8 trading sessions, we’ve seen days where Nvidia closed -9.5%, and +8.1% - with incredible high to low trading ranges, and as we see over the full-year Nvidia frequently sees 6%+ daily ranges. This is incredible movement for any company, let alone one with an almost $3t market cap, and along with its deep liquidity, and often strong underlying momentum and trending conditions, explains why traders are drawn to Nvidia as a trading vehicle above all other equity CFDs.

Pepperstone’s 24-hour Nvidia share CFDs – The new way to trade Nvidia

Pepperstone recently launched Nvidia 24-hour share CFDs.

Our Nvidia 24-hour share CFDs offer the ability for traders to trade Nvidia - long and short – and capture two-way opportunities during the traditional cash trading hours, the pre-and post-market sessions, but also when the traditional exchanges are closed through Asia. This makes for a continuous tradable price that offers traders the ability to react dynamically to headlines or sentiment shifts, at any stage through the trading week.

This continuous pricing also goes some way to reduce ‘gapping’ risk, which often occurs when the equity exchange re-opens. Where ‘gapping’ is one of the key risk’s traders face when holding positions through the closed period.

If impactful news breaks – be it, US election headlines, earnings announcements/guidance, key economic data or a central bank meeting – traders can capture opportunities or manage positions around the clock. With commission at 2c a share (no minimum commission), this costing structure means that traders can deploy a wide range of active trading strategies – in any size – discretionary or automated - and attempt to profit from two-way moves in the share price, while being able to effectively manage risk 24-hours a day.

Where to from here?

We’ve seen the arguments as to the investment case for Nvidia put forward by both the optimists and the doubters, and we can see that price action and the technical set-up reflects that debate. In my view, the stock is likely to trade a range for the period ahead, but which way it breaks will be fascinating to view and trade.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.