- English

- 中文版

It’s Not Only Geopolitical Hopes Driving The Equity Rally

History shows that equities seldom need a reason to rally, but almost always need a reason to roll over.

Handily, though, stocks do have plenty of reasons to rally at the moment, with tailwinds continuing to mount, even as we see record highs printed from Wall St to Tokyo.

Geopolitics Remain The Main Focus

We’ll address the obvious factor first, geopolitics.

To be clear, conflict in the Middle East is ongoing, and the Strait of Hormuz remains, for all intents and purposes, completely blocked. Though that is, at face value, a clear net negative macroeconomic factor, risk assets appear to have not only reconciled themselves with the inflationary impulse and growth headwinds that such an interruption to commodity flows will bring, but are also increasingly of the – in my opinion, correct – view that $100bbl oil shan’t cause the economic harm that it once might’ve done.

While there will, obviously, be a move higher in headline inflation on the back of higher energy costs, and some growth headwinds, the global economy, especially DMs, have moved to a considerably more diversified energy mix in recent years, while spending on energy as a proportion of overall consumption has also been in decline for some time. Added to which, fiscal policies are increasingly working to cushion against the impact of higher energy costs, amid various fuel subsidies and fuel tax tweaks here in Europe, along with tax refunds from last year’s OBBBA largely netting-off against higher energy spending stateside.

Setting the macro impact aside, participants, on balance, are also continuing to focus on the broader direction of travel from a geopolitical perspective, increasingly becoming desensitised to day-to-day headline noise.

At the time of writing, the overall path continues to be one that leads away from re-escalation, amid an indefinite extension of the US-Iran ceasefire, and towards some kind of deal being done to end the conflict, as talks between the two sides continue. While that path is likely to be a bumpy one, so long as we remain on it, risk appetite should remain underpinned.

AI Enthusiasm Makes A Resurgence

As noted, though, it is not only geopolitical optimism that is helping to propel risk assets higher.

For instance, we’ve seen, in the last couple of weeks, a marked resurgence in enthusiasm around the broader AI theme. Perhaps, the significant cheapening of tech valuations at the beginning of the conflict was enough to entice participants to re-up allocations to the sector, while solid earnings from the likes of TSMC, ASML, and Intel have likely also helped to reignite some of the euphoria on this front, ahead of next week’s megacap earnings where five of the ‘magnificent seven’ (AAPL, AMZN, GOOG/L, META & MSFT) are set to report.

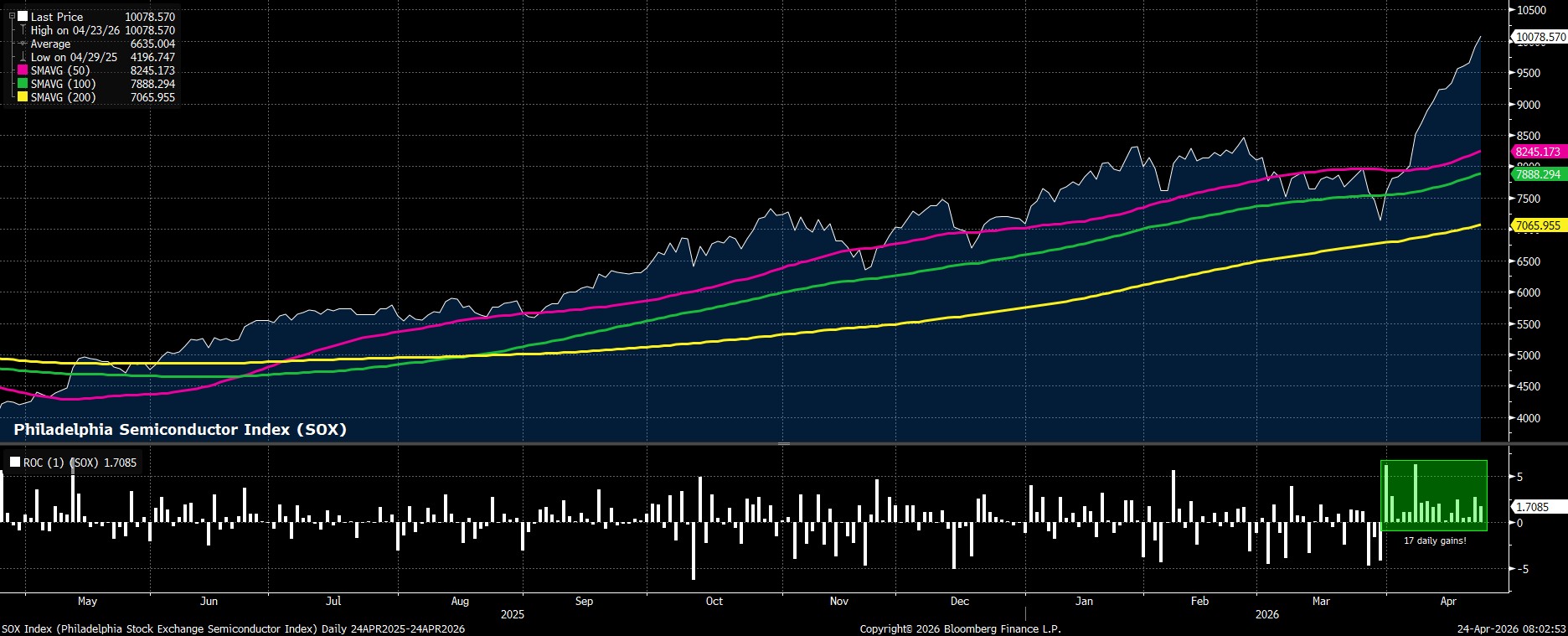

Altogether, these factors have driven the Philadelphia Semiconductor Index not only to a record high, but to an incredible 17-day winning streak. Considering the chunky weights that many of these names have in major equity benchmarks, this has hence dragged the broader market higher too.

Earnings Are Solid

Meanwhile, the underlying fundamentals of the market remain robust as well.

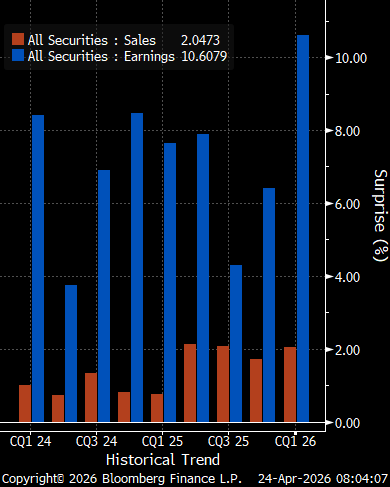

Around a quarter of S&P 500 firms have now reported Q1 earnings, and thus far reporting season has progressed very well indeed. Of those firms to have reported, not only have 80% surprised to the upside of consensus earnings expectations, but they have done so by the greatest magnitude in at least the last eight quarters. Furthermore, earnings growth is running at a double-digit YoY percentage for the sixth quarter in a row, while revenue growth is set for its fastest pace since Q3 22, just shy of 10% YoY.

While, of course, earnings could come under pressure in coming months as the macroeconomic fallout of conflict in the Middle East becomes clear, though that is clearly not yet the case, and on the whole guidance has been relatively robust. Consequently, this is all helping to further underpin risk appetite.

It is worth flagging, however, that while earnings performance on Wall St has been solid, it has been comparatively poor in Europe, with barely half of Stoxx 600 firms to have reported thus far managing to beat either sales or earnings expectations. This, coupled with Europe being more exposed to downside economic risks from higher energy prices, makes a return to ‘US outperformance’ seem logical, and thus long US/short Europe strategies seem appealing.

_Daily_2026-04-24_08-04-56.jpg)

Breadth A Reason To Worry?

Amid all this, it is worth flagging that concerns around ‘narrow breadth’ appear to have made a resurgence once more, in what has again been a widely hated, tech-led rally.

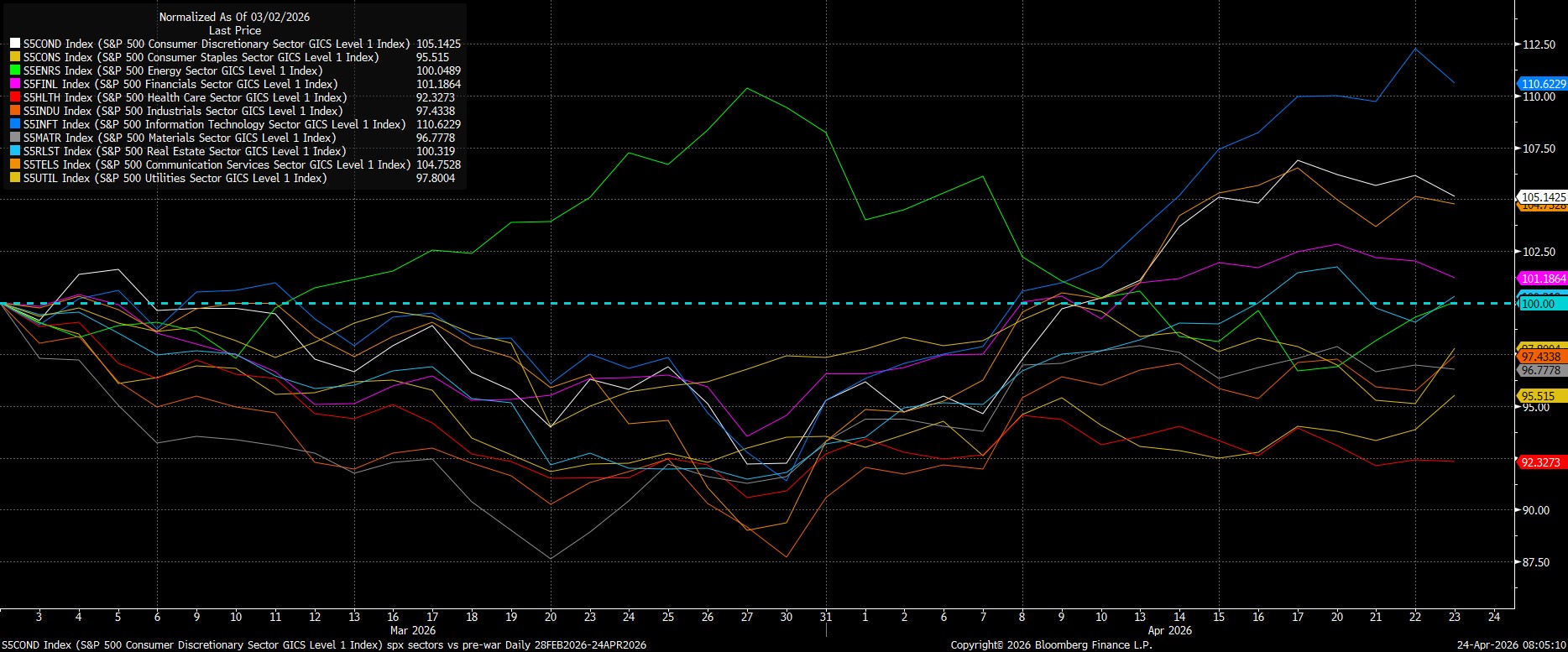

For context, only five of the S&P 500’s eleven sectors currently trade above their pre-conflict level, with Information Technology unsurprisingly leading the way. At a single-stock level, meanwhile, only 40% of index constituents trade above their February month-end close, while despite the benchmark having reclaimed its 200-day moving average almost three weeks ago, only around 60% of index members have achieved the same, compared to roughly two-thirds of members trading above that fabled yellow line at the back end of February.

While some may argue that this narrow market breadth is a potential sign of fragility, I’d actually argue the opposite, given that ‘bad breadth’ typically has little signalling value in terms of pointing to imminent market downside and, if anything, actually suggests that several sectors have ample room to ‘catch up’ with the rally that we’ve seen of late.

Conclusion

Wrapping up, while geopolitical hopes is an easy narrative on which to pin recent equity gains, it doesn’t tell the full story, given renewed tech-linked enthusiasm, and an increasingly solid fundamental backdrop. Consequently, while the geopolitical path continuing to lead towards de-escalation will help to underpin risk appetite, the solid earnings story should give participants further faith in the path of least resistance continuing to lead higher, and in dips remaining shallow for the time being.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.