July 2024 FOMC Preview: Setting The Stage For A September Cut

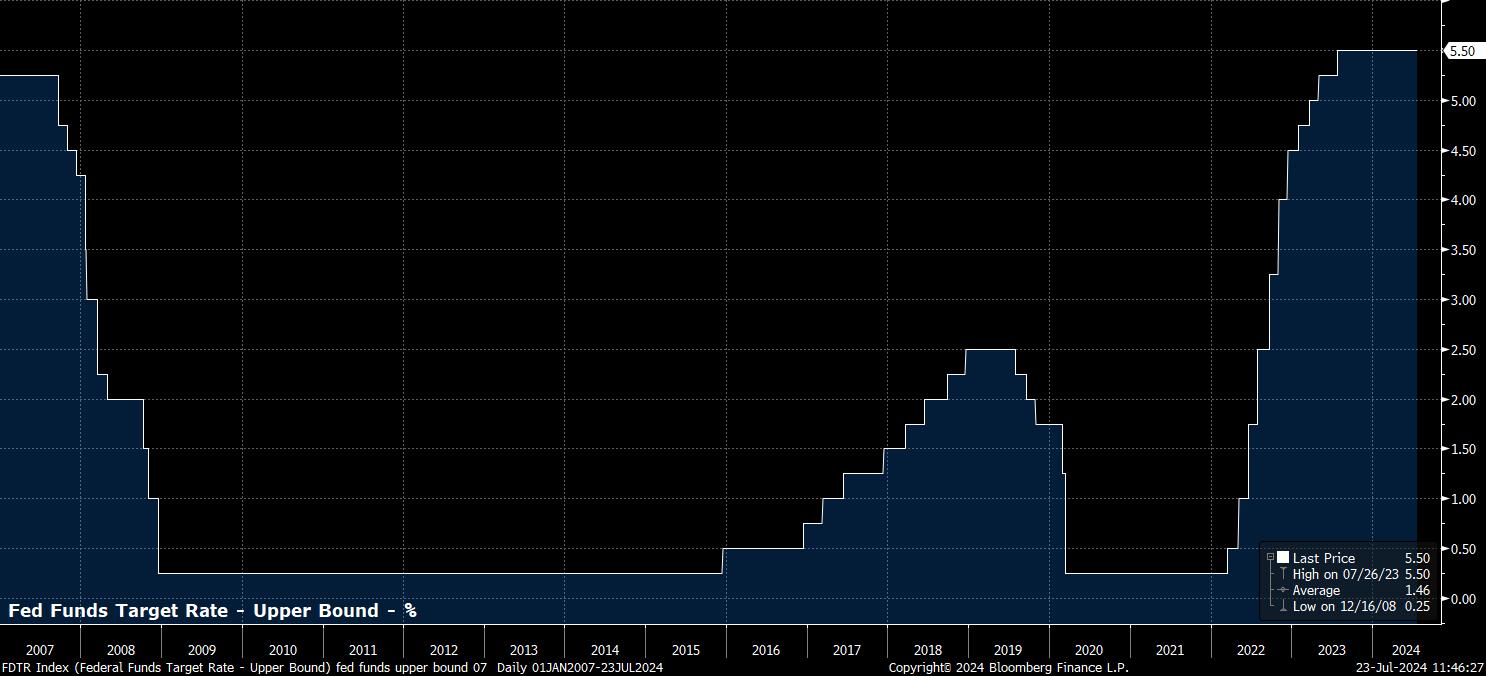

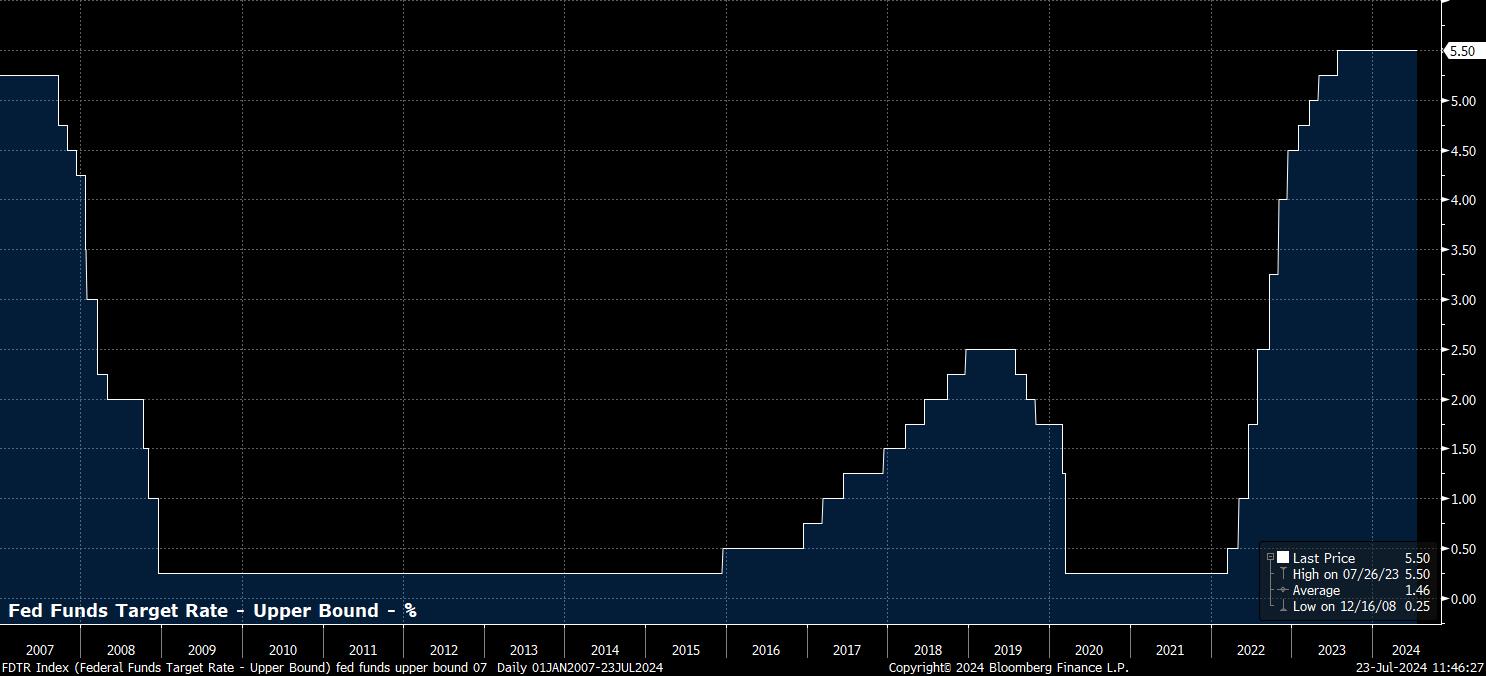

As noted, the target range for the fed funds rate is set to remain at 5.25% - 5.50% at the conclusion of the July policy meeting, in what should be a unanimous vote among FOMC members. This would mark not only the 8th consecutive meeting at which rates have been held steady, but also precisely a year since the fed funds rate reached its terminal level. Money markets, predictably, price next-to-no chance of any action at this meeting, with the USD OIS curve fully discounting the likelihood of rates remaining unchanged.

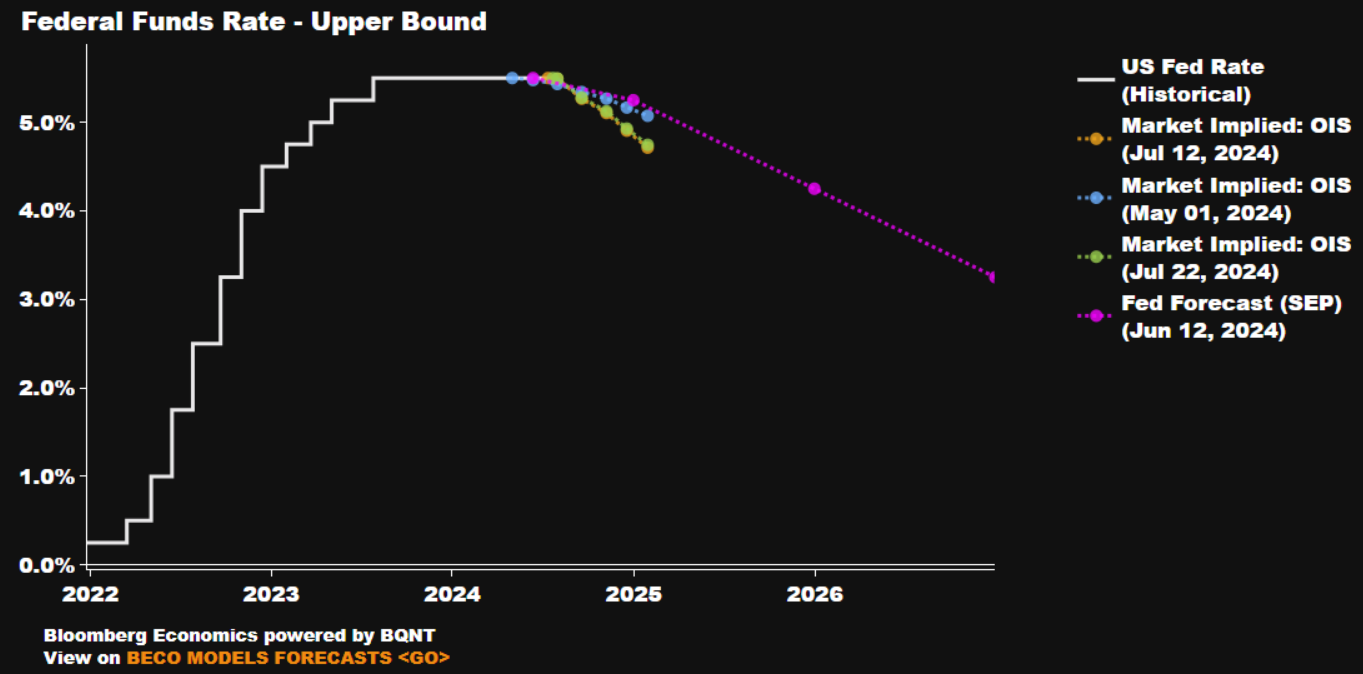

Further out, however, participants have become increasingly convinced that the FOMC will soon begin to remove some degree of policy restriction. The curve implies around an 87% chance that the first cut will be delivered by the time of the September meeting, while also pricing just over 56bp of easing, in total, by year-end. Of course, this is well over double the magnitude of easing implied by the median expectation in the June ‘dot plot’.

In any case, this is a significantly more dovish path than that priced prior to the June FOMC, at which markets viewed two cuts this year as just a 2-in-3 chance.

This repricing has been driven not only by data showing increased confidence in the disinflationary process, as well as signs of cracks emerging in the labour market – on which there is more below – but also by a continued tightening of the relative policy stance.

The real fed funds rate, using Chair Powell’s preferred calculation of subtracting from the fed funds rate the 1-year inflation breakeven, has risen to around 4.7%. Not only is this a significant rise from the 1.15% seen earlier in the second quarter, this also represents the highest real fed funds rate – and thus tightest policy stance – since the tail end of 2018; incidentally, just after Powell’s now-infamous remarks that quantitative tightening was on ‘autopilot’.

While rates are set to remain on hold, the policy statement should reflect the idea that rate cuts are on the horizon, likely as soon as the September meeting.

Although the FOMC are unlikely to explicitly pre-commit to any specific policy action, seeking to retain as much optionality as possible, with policymakers likely wanting to avoid being boxed in to any particular moves, there will likely be hints at near-term policy normalisation.

Firstly, the statement is likely to echo recent remarks from Chair Powell, in that the economy is beginning to make more substantial progress towards the inflation target, with the “modest” description of said progress from the June statement likely to be removed. Furthermore, it is likely that the July statement will also make mention of the increasing signs of fragility that are emerging in the labour market, noting that risks to the dual mandate of stable prices, and full employment, are now coming back into much better balance.

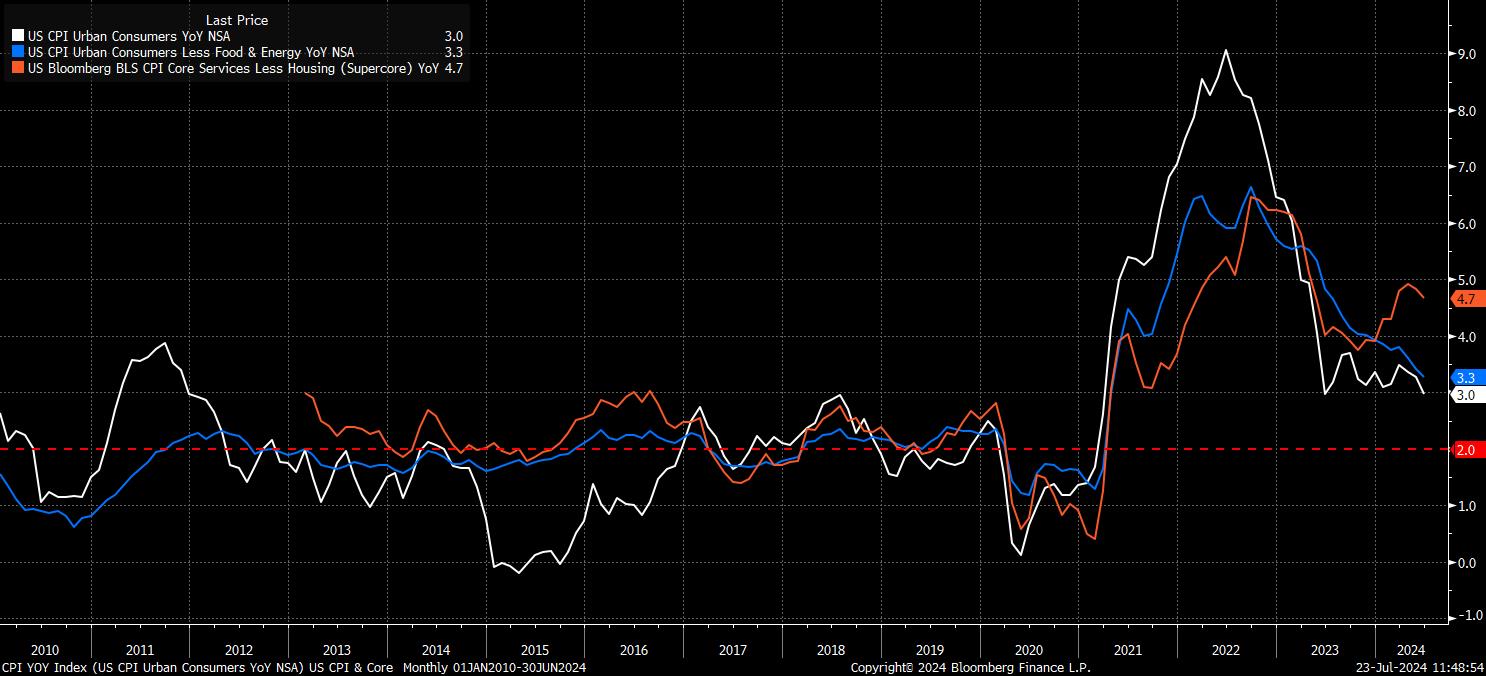

On that note, it is simple to see why the FOMC likely now possess an increased degree of confidence in inflation moving towards the 2% target. Headline CPI rose 3% YoY in June, its slowest annual rise in a year, while the index fell 0.1% on an MoM basis, the first monthly decline in prices seen since all the way back in May 2020, during the pandemic. Furthermore, core CPI rose just 3.3% YoY, its slowest annual increase since April 2021, while ‘supercore’ inflation notched a second straight monthly decline, to 4.7% YoY.

While these metrics all remain north of the 2% target, as does the Committee’s preferred core PCE metric at 2.6% YoY in May, it’s important to recall that policymakers are not seeking to achieve that target outright, instead simply wanting to obtain sufficient ‘confidence’ that said target will be achieved in a reasonable time period.

This owes to the well-documented ‘long and variable’ lags with which monetary policy impacts the economy, with Chair Powell himself having noted in a recent appearance that the Fed would’ve waited “too long” to cut rates if policymakers waited for 2% inflation to be achieved, potentially causing an undershoot of the inflation target as a result.

Meanwhile, on the labour market, a range of metrics show increasing signs of cracks emerging in what has, up to now, been a remarkably tight and resilient employment backdrop.

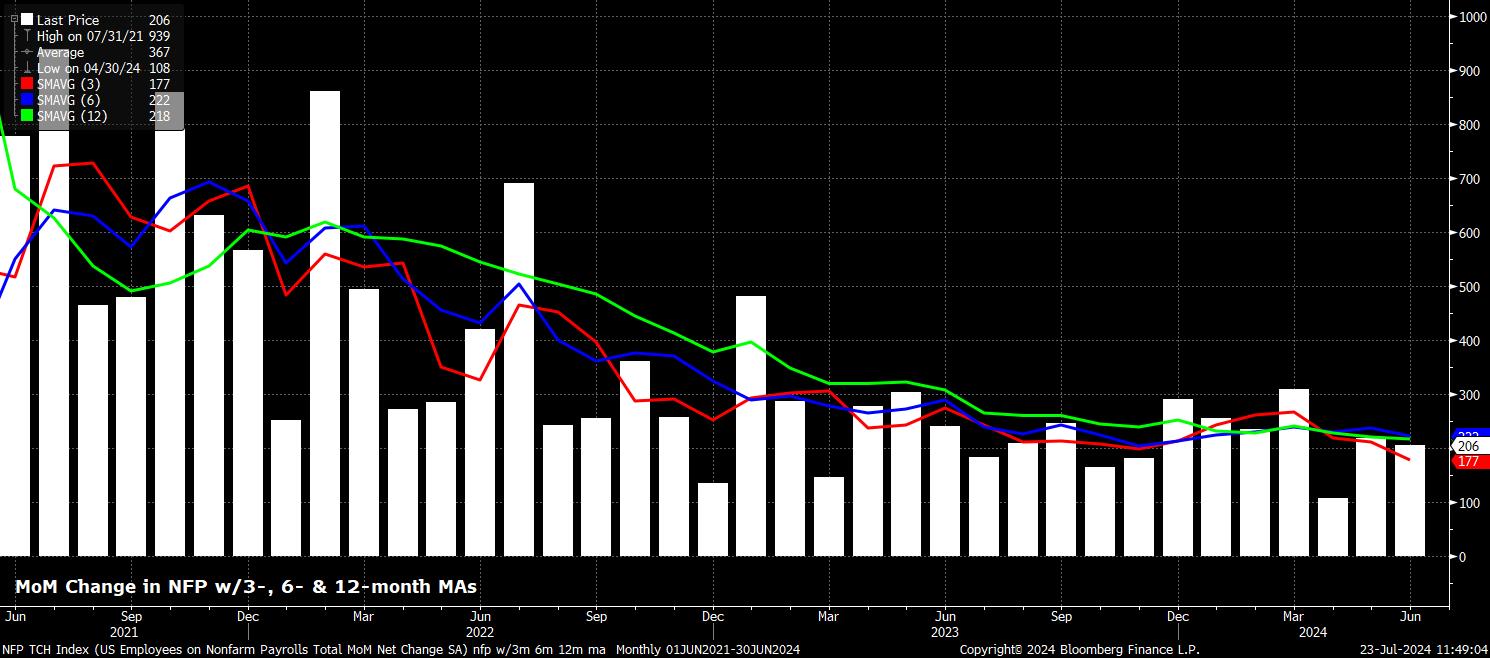

Headline nonfarm payrolls rose +206k in June, marginally above market expectations, however a sizeable net -111k revision to the prior two months’ worth of data drove the 3-month average of job gains to just +177k. Not only is such a figure considerably below the ‘breakeven’ pace of job gains, approx. 250k, which is required for growth in employment to keep pace with growth in the labour force, it also represents the lowest 3-month average of job gains since the beginning of 2021.

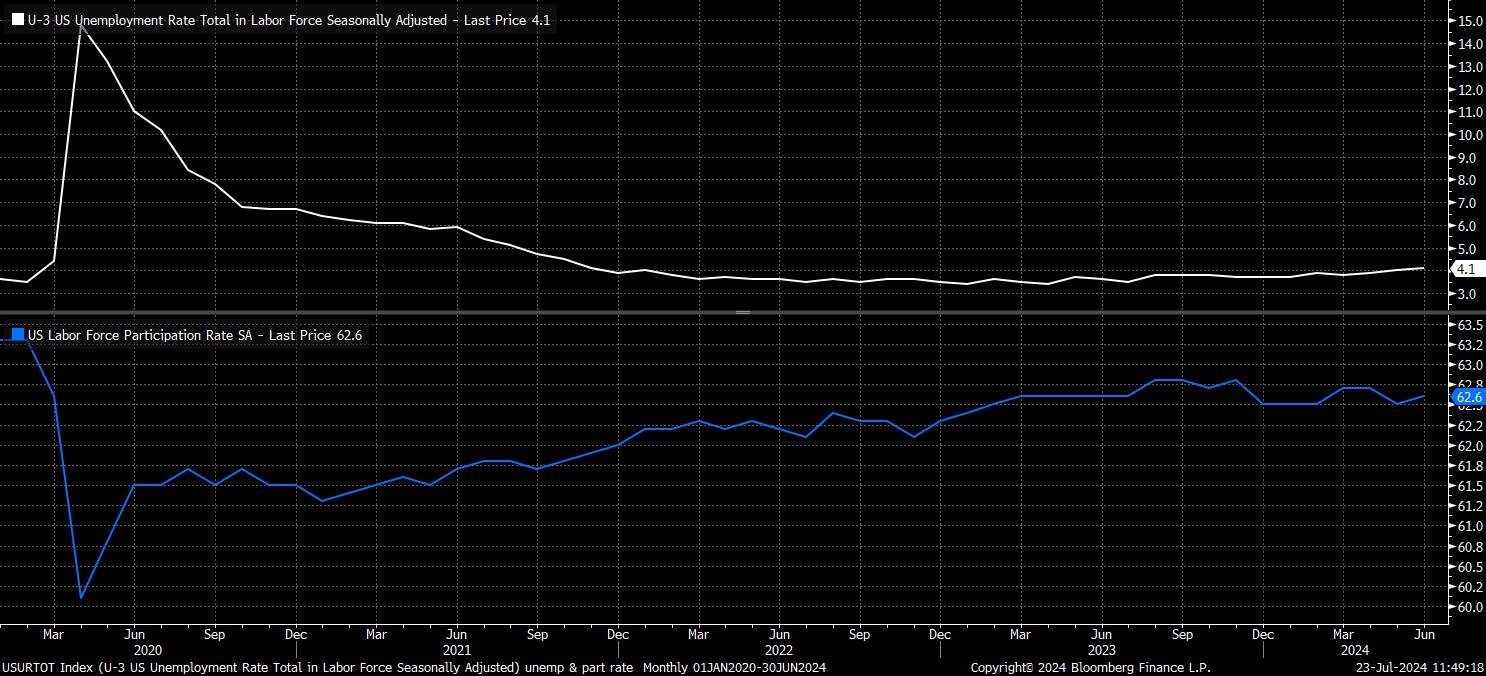

Meanwhile, unemployment rose to 4.1% in the same month, its highest level since November 2021, albeit an increase that came on the back of rising labour force participation. Nevertheless, further signs of cracks are also evident if one looks at initial jobless claims, which are currently running at a more than 2-year high, and continuing claims, which sit at the highest level since November 2021.

As Chair Powell noted recently, the labour market is now “essentially no tighter” than it was prior to the pandemic, at the time when the FOMC were delivering ‘insurance’ rate cuts, in the second half of 2019.

On the subject of Powell, his remarks at the post-meeting press conference are likely to be broadly in-keeping with those made recently, both in Congressional testimony, and subsequent speeches. Hence, Powell is likely to reaffirm that recent inflation prints have added to confidence in the disinflationary process, that risks to the dual mandate are now ‘two-sided’ in nature, and that inflation is no longer the sole risk that the Committee face. As noted earlier, pre-commitment to any future policy action is likely off the cards, while Powell will likely also play with a ‘straight bat’ any questions relating to the upcoming presidential election, and any impact it may have on the monetary policy outlook.

For markets, it is somewhat tough to envisage the USD OIS curve repricing further in a dovish direction. While strong signals of a September cut should be given, a cut which itself should kick-off the normalisation process, markets already discount a slightly more rapid pace of easing this year than the FOMC are likely to deliver, with three cuts in three meetings highly unlikely.

Nevertheless, any hawkish repricing is likely to be modest in nature, and shouldn’t pose too much of a headwind to equities, nor a tailwind to the USD. Instead, the July FOMC should re-affirm, and even strengthen, the long-running idea of the ‘Fed put’, which remains forceful and flexible in nature. This should, then, continuing to provide investors with confidence to remain further out the risk curve, leaving the path of least resistance pointing higher for equities, and seeing dips remain buying opportunities.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.